The UEMOA Banking Sector: A System Under Strain

The January 2026 economic outlook report for the West African Economic and Monetary Union (UEMOA) paints a sobering picture. While the regional banking sector has achieved notable milestones, it is increasingly undermined by a surge in financial risks. At the epicenter of this challenge stands Niger, whose staggering non-performing loan (NPL) rate has set a disturbing precedent for the entire union.

Niger: A Crisis of Proportions

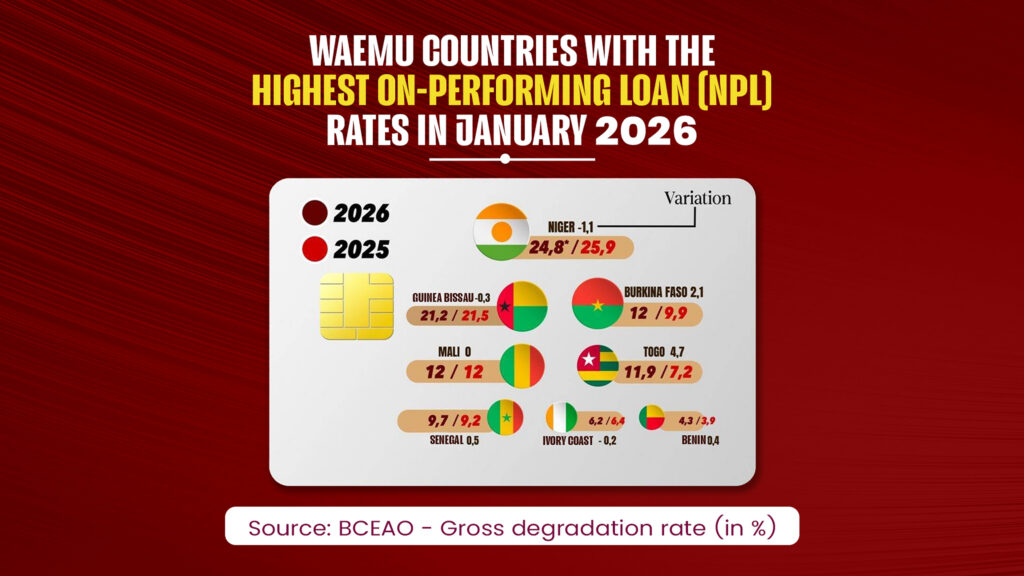

Despite marginal improvements in certain economic indicators, Niger remains the weakest link in the UEMOA banking chain. The country’s NPL ratio has reached an unprecedented 24.8% as of January 2026, signaling that nearly one in four loans granted in Niger is now in default. Although this figure represents a slight improvement from the 25.9% recorded in 2025, it starkly highlights the country’s structural vulnerabilities.

These vulnerabilities are exacerbated by persistent security challenges and political instability, which continue to erode investor confidence and loan repayment capacities. The gap between Niger’s NPL rate and the regional average underscores the severity of its predicament, positioning the country as a cautionary tale within the union.

A Tale of Two Regions: Coastal Strength vs. Sahelian Struggle

The latest data reveals a stark divide between the more resilient coastal economies and the beleaguered Sahelian bloc, where Niger serves as the crisis’s focal point.

The Sahelian Bloc: A Region in Freefall

Beyond Niger, other Sahelian nations are also grappling with alarming NPL rates:

- Mali and Burkina Faso: Both countries report NPL rates of 12%, with Burkina Faso experiencing a sharp increase of 2.1 percentage points over the past year.

- Guinea-Bissau: The country’s NPL rate stands at 21.2%, placing it dangerously close to Niger’s crisis levels.

The Coastal Bloc: Relative Stability with Exceptions

In contrast, the coastal nations demonstrate greater resilience, though not without their own concerns:

- Benin: Leading the union with the lowest NPL rate of 4.3%.

- Côte d’Ivoire and Senegal: Both maintain stable rates of 6.2% and 9.7%, respectively.

- Togo: An outlier in this group, Togo has seen its NPL rate surge from 7.2% to 11.9%, marking a dramatic increase of 4.7 percentage points.

Credit Growth Meets Rising Defaults

The UEMOA’s total credit portfolio to the economy has surpassed the 40,031 billion FCFA mark, reflecting a 4.7% annual increase. However, this growth is overshadowed by a troubling rise in bad loans, which now total 3,631 billion FCFA. The coverage ratio has plummeted to 59%, indicating that banks are struggling to keep pace with the escalation of defaults.

Banks Retreat: Tighter Lending Conditions

In response to the deteriorating risk profiles in high-default regions like Niger, banks are adopting a more cautious stance:

- Stricter lending criteria: Higher personal contributions and more stringent collateral requirements are now standard.

- Selective expansion: Banks are prioritizing balance sheet security over credit growth, potentially stifling financing for local SMEs and SMEs.

As the UEMOA banking sector navigates this critical juncture in early 2026, the situation in Niger and the ripple effects across the Sahel demand heightened vigilance. While the union’s overall financial stability remains intact for now, the risk of a liquidity crisis looms large if proactive measures are not taken to address the growing disparities and mounting defaults.